Market Update: 2024 Q4 in Review

Following is recap of stock and bond market performance through the end of the 3rd quarter along with our latest thoughts on the economy and markets, and how it may impact your retirement planning.

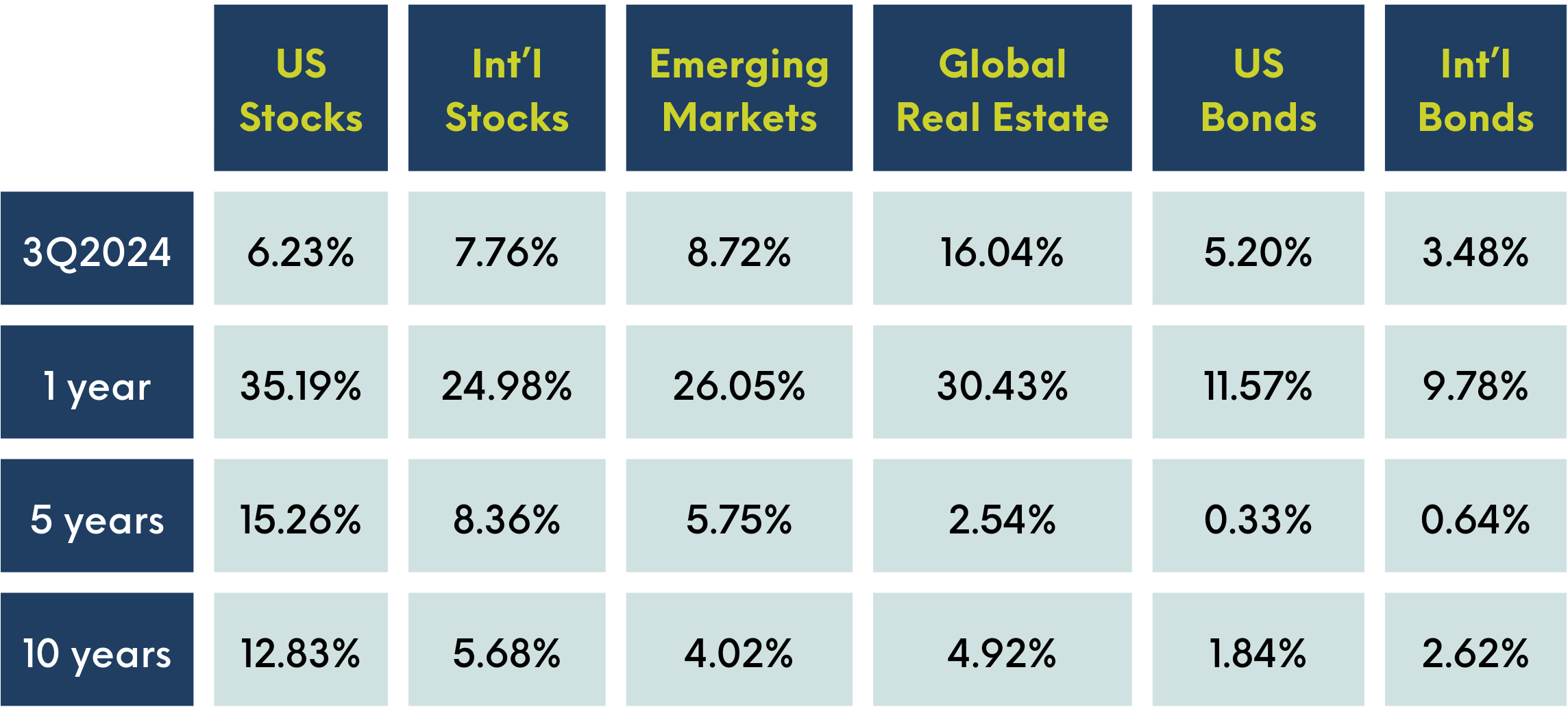

Past performance is not a guarantee of future results. Indices are not available for direct investment. Index performance does not reflect the expenses associated with the management of an actual portfolio. Market segment (index representation) as follows: US Stock Market (Russell 3000 Index), International Developed Stocks (MSCI World ex USA Index [net dividends]), Emerging Markets (MSCI Emerging Markets Index [net dividends]), Global Real Estate (S&P Global REIT Index [net dividends]), US Bond Market (Bloomberg US Aggregate Bond Index), and Global Bond Market ex US (Bloomberg Global Aggregate ex-USD Bond Index [hedged to USD]). S&P data © 2024 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. MSCI data © MSCI 2024, all rights reserved. Bloomberg data provided by Bloomberg.

THE ECONOMY

The U.S. economy remains solid with a lowered risk of recession.

After a slow start this year, the economy appears to have stayed on track with a solid growth pace over the summer, helped by consumer spending. This year has turned out as good as we could have hoped, returning to more of a “normal” economy with inflation down to around 2.5%, with similar expectations for next year. That said, it is an election year and there is also a high level of geopolitical tension. These stressors combined do pose risks to the economy, and so we are not completely out of the woods for a potential recession.

The job market remains on solid ground.

The job market appears to be returning more to “normal” after the post-pandemic boom, with job openings and quits back near pre-pandemic levels. That said, job openings are still higher than in any month prior to the pandemic, and data on layoffs and unemployment claims indicate that businesses have enough confidence to retain their workforce. Overall, while normalizing, the job market still looks healthy.

A cooling job market should contribute to lower inflation

While layoffs near historic lows suggest the rise in unemployment may just be a sign of the job market normalizing, it has helped slow wage growth. As job markets continue to cool, slower wage growth should contribute to lower inflation.

The global economy is improving, but not evenly.

The global economy has improved from last year's sluggish pace, but there are regional differences. Manufacturing remains slow in Europe and domestic demand in China has been weak. However, other parts of Asia are benefitting from investments in AI and other advanced technologies. With many global central banks focused on lowering interest rates, renewed economic momentum should position this year to be a solid one for the global economy, which has managed to avoid recession so far.

INFLATION & INTEREST RATES

Inflation is on a sustainable path back toward the Federal Reserve’s 2% target.

Cooling inflation allowed the Fed to join other global central banks in easing policy and deliver a 50-basis point rate cut in September. While the Fed’s updated projections forecast two more rate cuts this year, the pace of cuts will depend heavily on the incoming data. While inflation in housing and auto insurance remain high, the data continues to point to easing price pressures ahead. Slowing wage growth and a stable supply chain suggest that inflation is on a sustainable path back to 2%.

US STOCKS

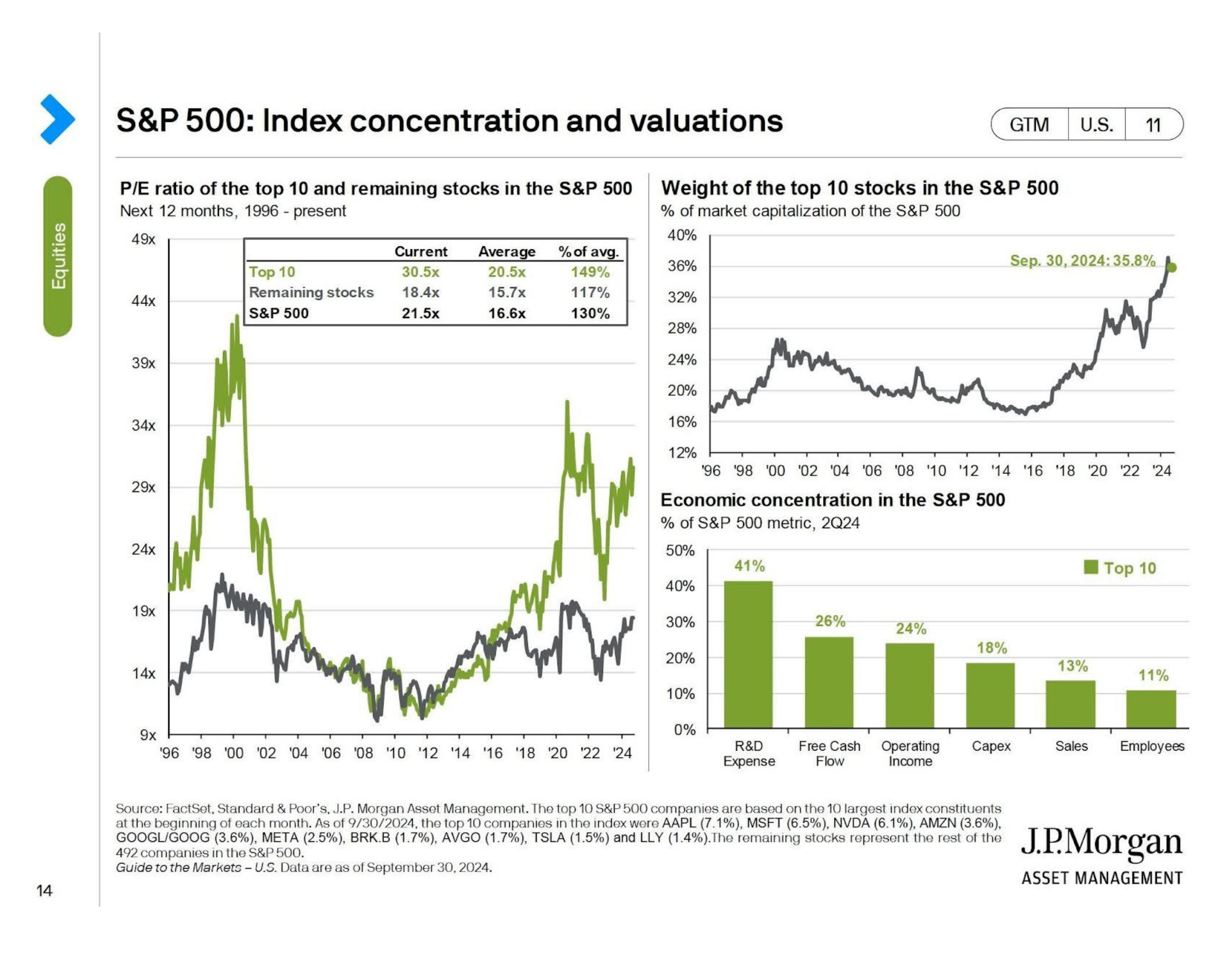

US equity markets are still concentrated in the largest stocks.

This summer was anything but calm in the markets. Stock volatility spiked in August due to lackluster performance from the Magnificent 7 (Apple, Microsoft, Google, Amazon, Meta, Tesla, and Nvidia), weaker economic data, and policy action from the Bank of Japan. The markets have been on a tear as of late, however, and resilient economic activity and earnings growth above 10% has sent U.S. stocks higher. Importantly, the rally has extended to a broader group of stocks, outside of the most dominant companies just mentioned.

Although US stocks have returned approximately 50% since the beginning of 2023, the gains have been heavily concentrated among the largest 10 stocks which currently make up over 35% of the S&P 500 Index. A quick look at the top left corner of the below chart will show the steep prices of these 10 stocks. Lower than expected earnings for this group could have an oversized impact on your portfolio on the downside as well, reminding us of the importance of a well-diversified portfolio. Also importantly, if the economy continues its steady growth, gains should continue to broaden out to other parts of the market, rewarding diversification.

BONDS

Current bond yields still look attractive.

Bonds were up over 5% during the 3rd quarter based on expectations of a rate cut. While yields across the fixed income market have fallen, they are still trading above their 10-year medians in many sectors. With current yields likely to fade as the Federal Reserve cuts rates further, investors may want to take advantage of attractive levels of income while they still can.

INTERNATIONAL EQUITIES

International stocks look well priced compared to the US.

A long cycle of U.S. stocks outperforming international markets has left many U.S. based investors nervous about allocating abroad and left many over-exposed to domestic equities. While U.S. stock market performance has been impressive, the performance has driven this over concentration in global equity indices to an all-time high of 64%. This heavy concentration exposes investors to risks specific to U.S. markets, including elevated valuations.

Despite a volatile third quarter, international stocks have maintained their upward momentum, and many markets are up over 10% this year. Even so, international markets continue to look attractively priced compared to the U.S. This, combined with improving fundamentals, structurally higher interest rates and a more favorable economic outlook, makes investing abroad attractive.

WHAT IT ALL MEANS

As always, let us translate this into what this means for your retirement savings:

Don’t let volatility (or the best performing funds) distract you from fundamentals.

Diversification rules and so does the adage to “buy low, sell high”. This means that investing only in the current market darlings is probably not your best long-term bet, and it’s also important to KEEP investing when markets are down. Read more here about dollar-cost averaging and how it can help your portfolio.

Diversification is the key to long term retirement planning success.

If you are worried you are being too aggressive (or not enough), now is the time for a review of your portfolio. An appropriate allocation is dependent on a variety of factors including how much you have saved (and are still saving), your current financial situation and goals, and your expectations for retirement.

Get help if you need it.

If you have questions or would like to touch base on your retirement planning, please call or schedule a meeting with us.

We’re here to support you.

Best regards,

Katrina & Team

Katrina Bell, CIMA®

Book a call: https://calendly.com/katrinabell/30mincall

M: 503-891-8319

3903 S. Kelly Avenue, Portland, OR 97239

ZUNA is a registered investment adviser, registered with the Securities and Exchange Commission. Advisory services are only offered to clients or prospective clients where ZUNA and its representatives are properly licensed or exempt from licensure. The information contained in this electronic mail message, including any attachments, is confidential and intended solely for the use of the person or entity to whom the e-mail is addressed. Any further distribution of this message is prohibited without the written consent of the sender. If you are not the intended recipient of this message, be advised that any dissemination, distribution, copying or use of the contents of this message is strictly prohibited. If you received this e-mail message in error, please contact the sender by reply e-mail. Also, please permanently delete all copies of the original e-mail and any attachments.

Source: JP Morgan, Dimensional Fund Advisors